Business fraud claims cost companies billions annually, yet many owners don’t recognize the warning signs until significant damage occurs. At The Law Offices of Alan J. Carnegies, APC, we help Los Angeles County businesses detect fraud early and build defenses that protect their interests.

This guide walks you through the most common fraud schemes, the red flags to watch for, and the strategic steps needed to defend your company effectively.

What Fraud Schemes Cost Your Business Most

Asset Misappropriation Remains the Leading Threat

Embezzlement represents the most destructive fraud threat facing Los Angeles County businesses. The Association of Certified Fraud Examiners reported in 2024 that asset misappropriation-the direct theft of company funds or assets-accounts for nearly 89% of all business fraud cases, with an average loss of $120,000 per incident. This isn’t theoretical damage. A single employee with access to financial systems can drain accounts before detection occurs.

Payroll fraud inflates the problem further, with schemes ranging from ghost employees to falsified overtime records that cost companies thousands to millions annually.

Financial Statement Fraud and Misrepresentation

Financial statement fraud operates differently but causes equal harm. When business owners misrepresent revenues or hide liabilities during mergers, acquisitions, or vendor negotiations, they create artificial valuations that mislead investors and distort stock prices. Misrepresentation in business transactions extends beyond financial statements into concealment of pending lawsuits, regulatory violations, or undisclosed liabilities that fundamentally alter deal economics. Procurement fraud through vendor kickbacks and invoice inflation undermines fair competition and inflates costs systematically.

Investment Fraud and Ponzi Structures

Investment fraud schemes like Ponzi structures promise unrealistic returns funded entirely by new investor money rather than legitimate business operations-eventually collapsing and destroying investor capital entirely. These schemes operate on deception from inception and leave victims with substantial losses.

Immediate Response Protects Your Recovery

The practical defense begins with immediate action when fraud is suspected. Preserve all relevant documents and communications before they disappear or are destroyed. Data analytics applied to financial transactions reveal anomalies that manual review misses-unusual payment patterns, duplicate invoices, or transactions outside normal business cycles signal trouble. Forensic accounting quantifies actual losses and establishes the timeline of fraudulent activity, which courts require for damage awards. Early involvement of counsel protects your company’s ability to recover losses and prevents further damage from continuing schemes.

Understanding what fraud costs your business sets the foundation for recognizing the warning signs that appear before major losses occur.

Spotting Fraud Before It Destroys Your Bottom Line in Calabasas, California

Detecting Unusual Financial Patterns

Fraudsters operate deliberately to avoid detection, which means you need systematic methods to catch what they hide. Unusual financial patterns reveal themselves through specific indicators that standard accounting reviews often miss. Duplicate invoice payments to the same vendor, payments to vendors with similar names to legitimate suppliers, or transactions processed outside normal approval workflows all signal trouble. Data analytics applied to your accounting system flags these anomalies automatically-transactions that deviate from established patterns, unusual payment sizes compared to historical norms, or accounts receivable aging that doesn’t match your business cycle. The Association of Certified Fraud Examiners reported in 2024 that organizations using continuous auditing and data analytics detected fraud schemes 24 months faster than those relying on periodic audits alone.

Monthly bank reconciliations rather than quarterly ones create accountability that prevents fraudulent transfers from hiding in gaps. Credit card statements require line-by-line review for personal expenses, unusual merchant categories, or patterns inconsistent with business operations. Payroll systems need duplicate Social Security number checks across employee records-ghost employees often use variations of real names or addresses to bypass initial screening. Cross-reference vendor addresses against employee addresses; procurement fraud frequently involves kickback schemes where employees control both sides of the transaction.

Identifying Document Irregularities

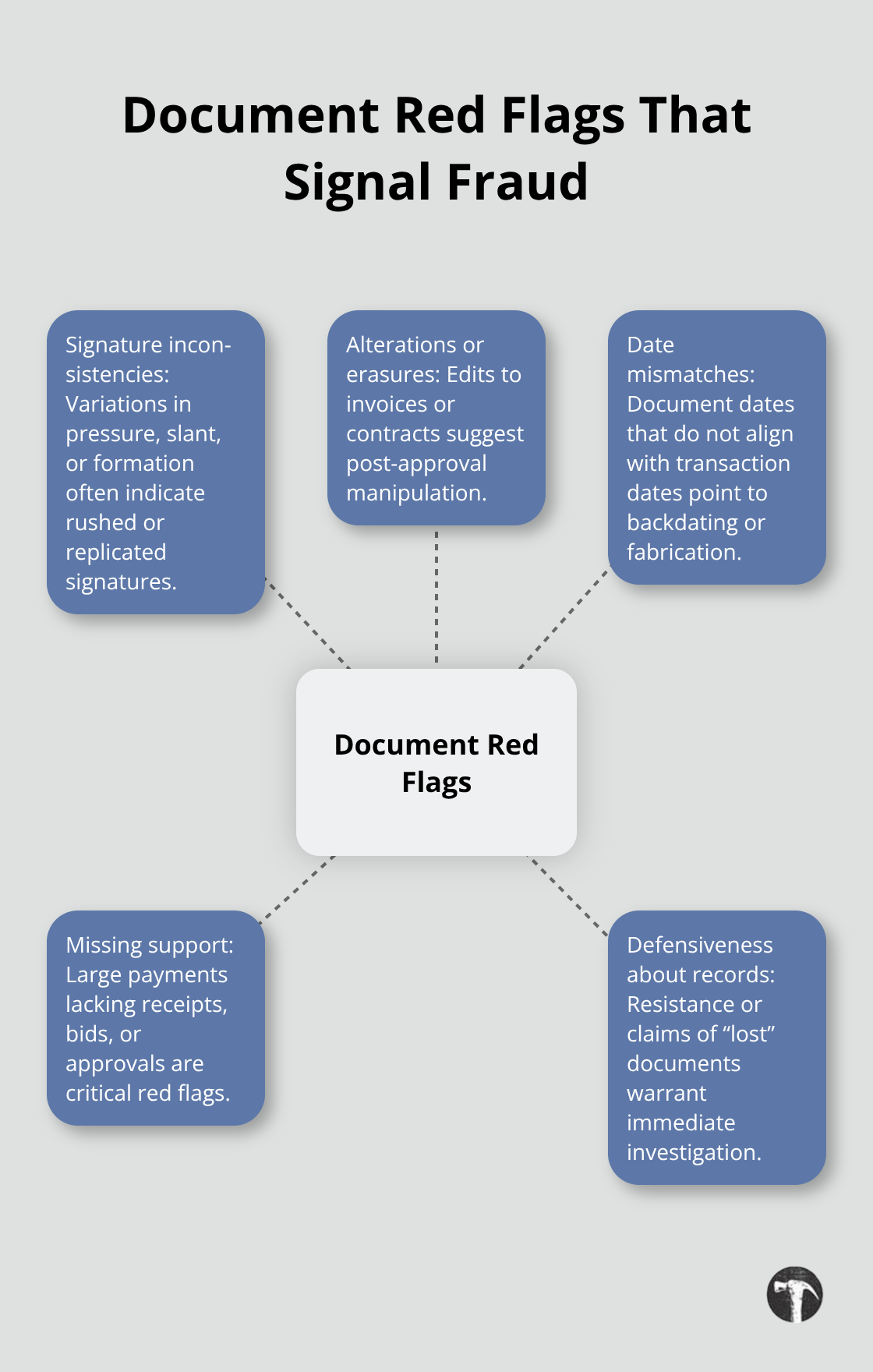

Document irregularities signal calculated deception more reliably than financial anomalies alone. Signatures on checks, contracts, and authorizations reveal inconsistencies when fraudsters rush or grow careless with signature replication. Alterations to original documents, erasures on invoices, or mismatches between document dates and transaction dates expose manipulation. Missing supporting documentation for large purchases or payments represents a critical red flag; legitimate transactions leave audit trails.

When employees suddenly become defensive about requests for documentation or claim records were lost, investigate immediately rather than accepting explanations.

Recognizing Behavioral Red Flags

Behavioral changes often accompany fraud and warrant immediate attention. Increased defensiveness about financial inquiries, sudden resistance to vacation time that would expose unauthorized access, or unusual irritability when financial controls tighten all suggest hidden activity. Employees committing fraud frequently avoid delegating responsibilities because they need direct control over fraudulent transactions. Communication inconsistencies matter: statements that change when questioned, vague explanations for transactions, or reluctance to put decisions in writing all suggest someone protecting themselves from documented evidence.

Taking Action on Detection

The practical defense begins with immediate action when fraud is suspected. Preserve all relevant documents and communications before they disappear or are destroyed. Forensic accounting quantifies actual losses and establishes the timeline of fraudulent activity, which courts require for damage awards. Early involvement of counsel protects your company’s ability to recover losses and prevents further damage from continuing schemes.

Once you identify fraud indicators, the next critical step involves building a defense strategy that transforms evidence into legal remedies.

How to Build an Unshakeable Defense Against Fraud Claims in Calabasas, California

Preserve Documents Within Hours, Not Days

Document preservation must happen within hours of discovering fraud, not days or weeks later. Courts recognize that delayed preservation weakens your defense position because opposing counsel will argue you had time to manipulate or destroy evidence. Immediately halt normal document destruction protocols and issue a litigation hold notice to all employees instructing them to preserve emails, spreadsheets, communications, and physical records related to the suspected fraud. This step alone prevents opposing parties from claiming negligence in evidence handling.

Next, secure access to all financial systems and restrict changes to historical records. Most accounting software maintains audit trails showing who accessed what data and when modifications occurred. These digital timestamps become critical proof that you took fraud seriously and did not alter records after the fact. Gather bank statements, credit card records, vendor invoices, employee files, and communications with the accused party. Organize these materials chronologically rather than by category; chronological organization reveals patterns that categorical filing misses.

Forensic Accountants Quantify Losses With Precision

Hiring a forensic accountant within days of fraud discovery transforms scattered evidence into court-admissible damage calculations. Forensic accountants use specialized software to analyze thousands of transactions simultaneously, identifying patterns that manual review cannot detect. They reconstruct financial flows, trace funds through multiple accounts, and quantify exactly how much money the fraudster moved and where it went.

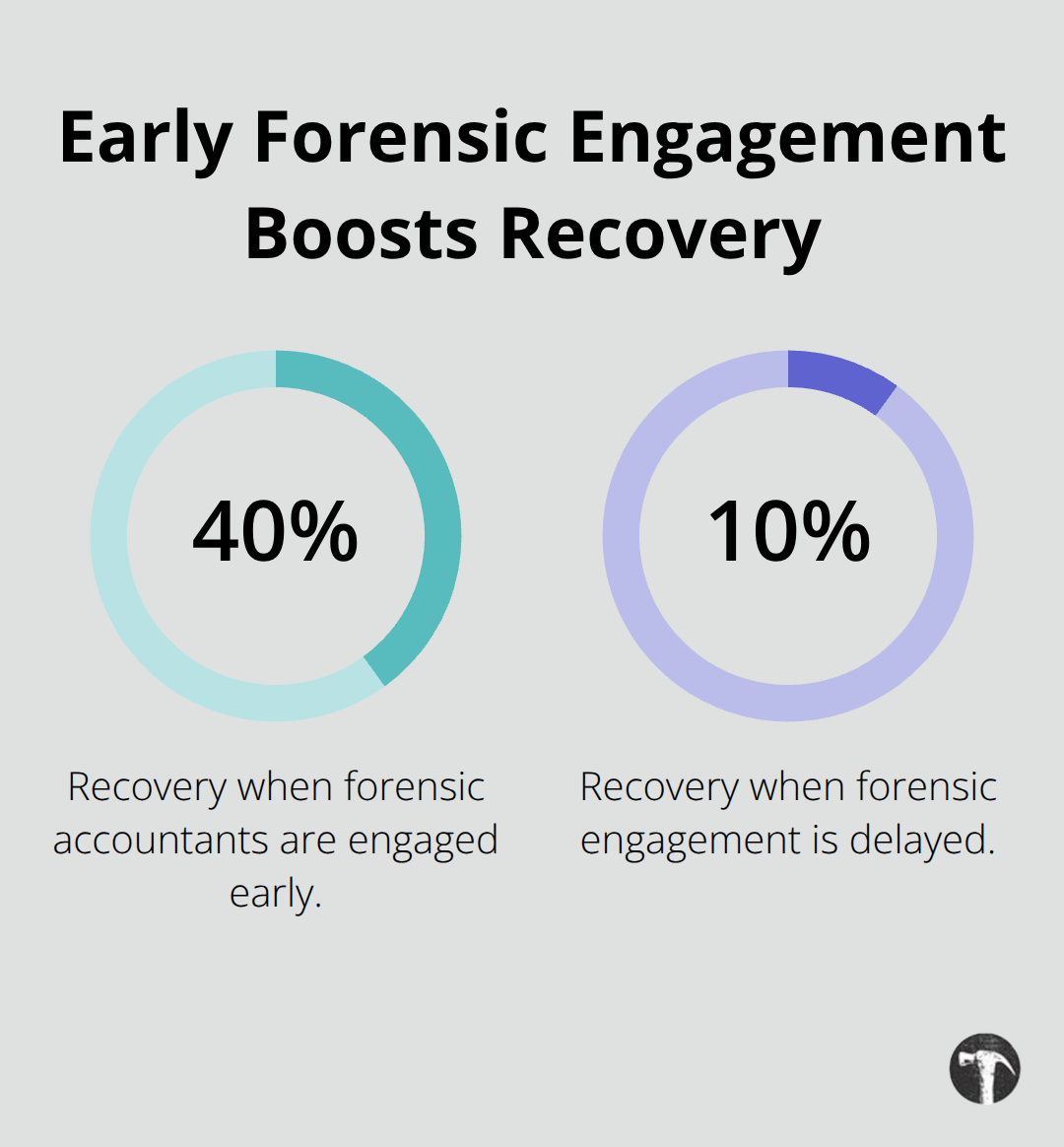

This quantification matters because Texas law requires you to prove actual damages with specificity; judges reject vague estimates of loss amounts. The Association of Certified Fraud Examiners found that organizations engaging forensic accountants early recovered approximately 40% of losses compared to 10% recovery for those who delayed. Investigators then use the accountant’s findings to conduct interviews and gather additional evidence.

They interview employees who worked with the accused party, examine communications for inconsistencies, and verify whether the fraudster had the access and opportunity to commit the crimes alleged. This combination of forensic accounting and investigative work creates a factual foundation that withstands courtroom scrutiny.

Timeline Construction Demonstrates Methodical Action

A detailed timeline of events demonstrates to courts that you acted methodically rather than emotionally or reactively. Start with the earliest suspicious transaction you can identify and work forward month by month, documenting what happened when. Include the date you discovered fraud, dates of specific fraudulent transactions, dates employees reported concerns, dates of internal communications about the suspected fraud, and dates you contacted counsel.

Timelines reveal whether fraud occurred over weeks or years, whether multiple employees participated, and whether management ignored warning signs that should have triggered investigation. A timeline showing management ignored obvious red flags for months strengthens claims of constructive fraud under Texas law. Conversely, a timeline showing you discovered and acted on fraud within days demonstrates reasonable business practices and limits exposure to punitive damages claims. Include dates of all document preservation efforts, forensic accounting engagement, and investigator involvement. Courts view this proactive documentation as evidence of good faith.

The timeline also identifies the statute of limitations deadline for your fraud claims. Texas law provides a four-year window for business fraud claims under Section 27.01, so knowing exactly when fraud began determines when you must file suit. We at The Law Offices of Alan J. Carnegies, APC help Los Angeles County businesses establish these timelines and protect their legal rights within the applicable deadlines.

Final Thoughts

Business fraud claims demand immediate action once you suspect deception. The detection methods outlined above-monitoring financial patterns, examining documents for irregularities, and recognizing behavioral changes-form the foundation of effective defense. Organizations that implement continuous auditing and data analytics catch fraud 24 months faster than those relying on periodic reviews alone, and Texas law provides a four-year window for business fraud claims under Section 27.01, but this deadline moves quickly.

Document preservation within hours of discovery, forensic accounting engagement, and detailed timeline construction transform scattered evidence into court-admissible proof of damages and intent. Courts require specific damage calculations rather than estimates, which means forensic accountants must quantify losses with precision from the start. Investigators must verify opportunity and access before memories fade or witnesses become unavailable, and delays in filing suit or gathering evidence weaken your position substantially.

We at The Law Offices of Alan J. Carnegies, APC represent business owners throughout Los Angeles County facing fraud disputes. Our approach combines immediate evidence preservation with forensic analysis and strategic litigation planning to help you understand your legal options, quantify recoverable losses, and pursue remedies that protect your business interests. Contact us today to discuss your situation and learn how we can help protect your business from ongoing fraud exposure.